Decoding the Sec. 530A “Trump” Account & The Colorado 529 Strategy

For parents looking to maximize wealth transfers to the next generation, a brand-new tax vehicle has emerged alongside a powerful, localized staple. The Section 530A “Trump” Account (TA)—set to go live after July 4, 2026—is a game-changing “starter” retirement vehicle designed specifically for minors. By pairing it with a Colorado CollegeInvest 529 Plan, parents can build an unbeatable, dual-track savings strategy covering both education and retirement.

Actionable Items for Parents

- Claim the Federal “Free Money”: If your child is a U.S. citizen born between 2025 and 2028, elect the automatic $1,000 federal Pilot Program contribution via Form 4547 or trumpaccounts.gov.

- Activate Your Account: BNY/Robinhood will issue account activation instructions. Complete these early so your child’s account is live right after the July 4, 2026 launch.

- Utilize the Gift Tax Workaround: To avoid filing Form 709 gift tax returns for direct third-party TA contributions, deposit cash into a standard custodial savings or investment account first, then transfer it into the TA.

- Capture the Colorado State Tax Deduction: Ensure your 529 contributions are made to a state-administered CollegeInvest account by December 31 to lower your Colorado taxable income.

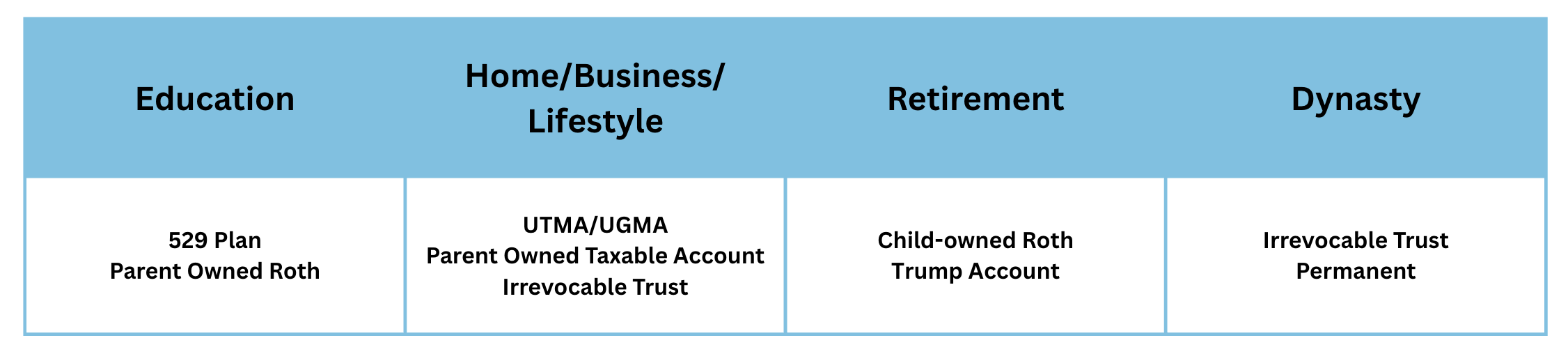

What is the best account for the goal you have?

Main Takeaways

- Two Distinct TA Phases: A Trump Account restricts all distributions during its “Growth Period” (birth through age 17). Post-age 18, the child gains full withdrawal capability and can choose to convert the account to a Roth IRA.

- Rigid Investment Guardrails: To protect compounding minors, TA growth period investments are restricted to U.S. equity market-cap index funds with annual fees capped at a razor-thin 0.10% (10 bps).

- Unmatched Colorado State Deductions: Colorado offers exceptionally high state income tax deductions for 529 plan contributions, directly reducing a family’s state tax liability.

Detailed Breakdown of the Rules

1. The Sec. 530A Trump Account Mechanics

The Trump Account allows up to a combined $5,000 per year (indexed for inflation after 2027) in direct and pre-tax employer contributions. Unlike traditional IRAs, the annual deadline for a TA contribution is strictly December 31 of the calendar year.

During the minor’s upbringing, the funds grow tax-deferred at the federal level. However, local state tax rules vary. Colorado families should note that Colorado is not currently listed among the states planning to tax annual internal TA earnings (unlike California, Hawaii, or Massachusetts), making it a highly tax-efficient vehicle for Coloradans.

Once the beneficiary reaches their age-18 year, they can roll the account over or execute a Roth conversion. While conversions trigger income tax on the earnings, it sets the child up with completely tax-free retirement growth for life. Beware the Kiddie Tax: if you convert large sums while the child is a student under 24, earnings above $2,700 will be taxed at the parents’ marginal tax rate.

2. Supercharging with the Colorado 529 Plan

While the Trump Account builds a fortress for retirement, college and trade school expenses are best handled by Colorado’s CollegeInvest 529 program.

- The Tax Benefits: For the 2026 tax year, Colorado taxpayers can deduct up to $26,200 per beneficiary for single filers, or $39,200 per beneficiary for joint filers, directly from their state income tax returns.

- The Lifetime Cap: Families can accumulate a massive lifetime maximum of $500,000 per beneficiary across all Colorado 529 accounts.

- Flexibility: Earnings grow 100% federal and state tax-free when used for tuition, books, computers, and housing. If your child skips college, you can roll up to $35,000 of lifetime unused 529 funds into a Roth IRA (subject to SECURE 2.0 rules) or switch the beneficiary to another family member penalty-free.