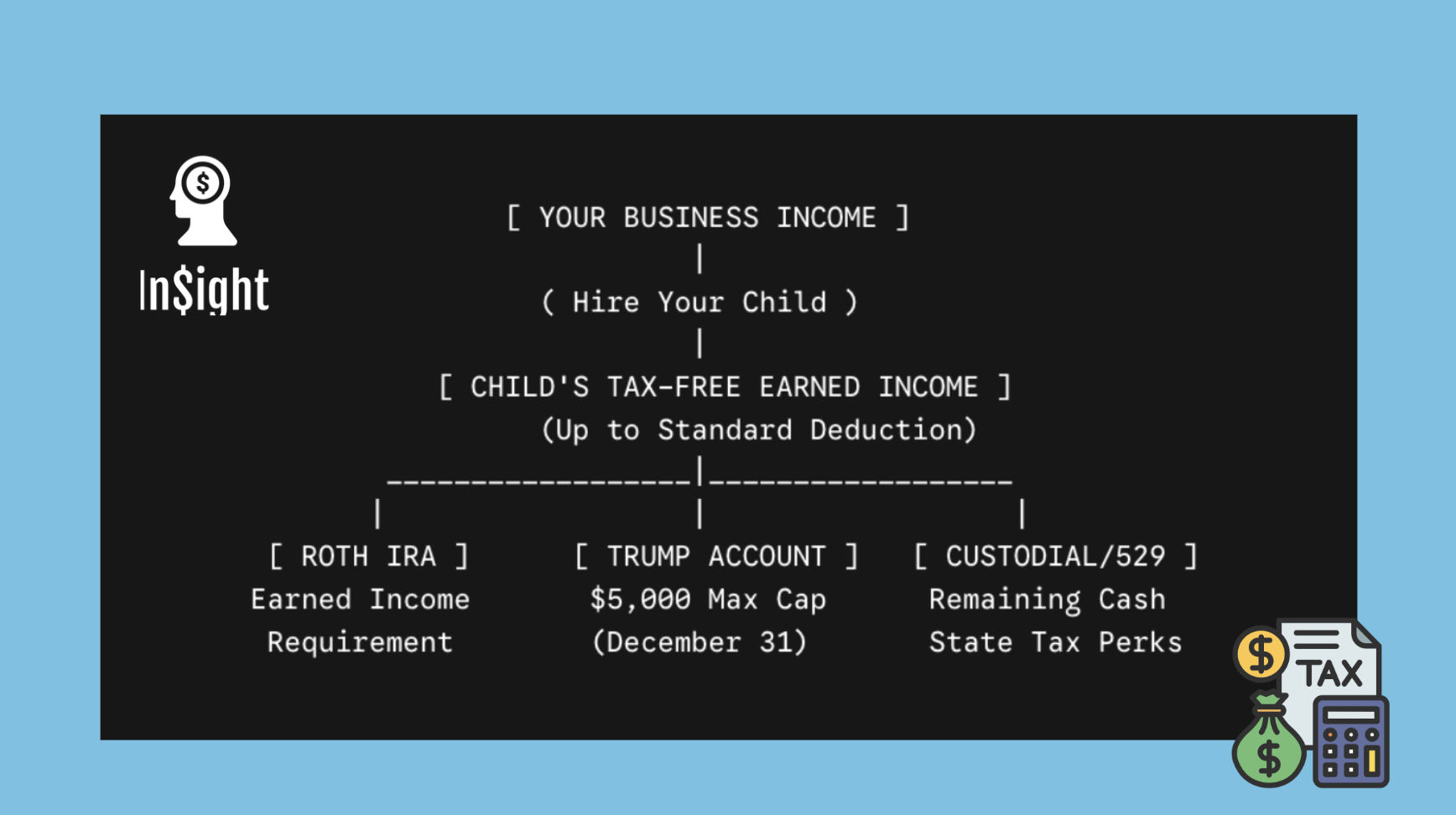

If you are a business owner or independent contractor, you possess a legal financial superpower: the ability to hire your children. By shifting business income to your kids, you can completely wipe out a portion of your tax burden while simultaneously fully funding a Trump Account, 529 Plan, Roth IRA, and Custodial Account (UTMA).

Here is how self-employed parents can stack these four vehicles to optimize savings, taxes, and intergenerational wealth.

The Legal Foundation: Legitimate Earned Income

To make this matrix work, your child must do legitimate work for your business (e.g., modeling for marketing, cleaning office space, managing social media, data entry) and be paid a reasonable, market-rate wage.

If your business is a Sole Proprietorship or a single-member LLC taxed as a sole proprietorship, wages paid to your children under age 18 are exempt from FICA (Social Security and Medicare) taxes. Furthermore, under the federal standard deduction, your child can earn up to a certain threshold completely free of federal income tax, while your business claims a 100% deduction for their wages.

How to Fund and Stack the 4 Vehicles

Once your child has tax-free earned income in their own bank account, you can deploy the capital across these four structures:

1. The Child-Owned Roth IRA (The Growth Engine)

- The Rule: A child can contribute 100% of their earned income up to the annual limit into a Roth IRA.

- The Strategic Benefit: Because the child’s tax bracket is essentially 0%, they pay no tax on the money going in, and the funds grow entirely tax-free for their lifetime. Unlike the Trump Account, a Roth IRA allows the child to withdraw their contributions (the principal) at any time, completely penalty-free, offering excellent flexibility for early adulthood.

2. The Sec. 530A Trump Account (The Pre-18 Lockbox)

- The Rule: Anyone can contribute up to $5,000 per year into a child’s TA during the growth period.

- The Strategic Benefit: Because the child has earned income, your business can actually execute Sec. 128 Employer Contributions of up to $2,500 directly into their Trump Account. This is an above-the-line federal tax exclusion for the business. The remaining $2,500 can be swept in as a direct contribution from their earned savings to hit the $5,000 combined limit. This cash is locked tightly until they turn 18, ensuring parents can build an un-touchable compounding nest egg.

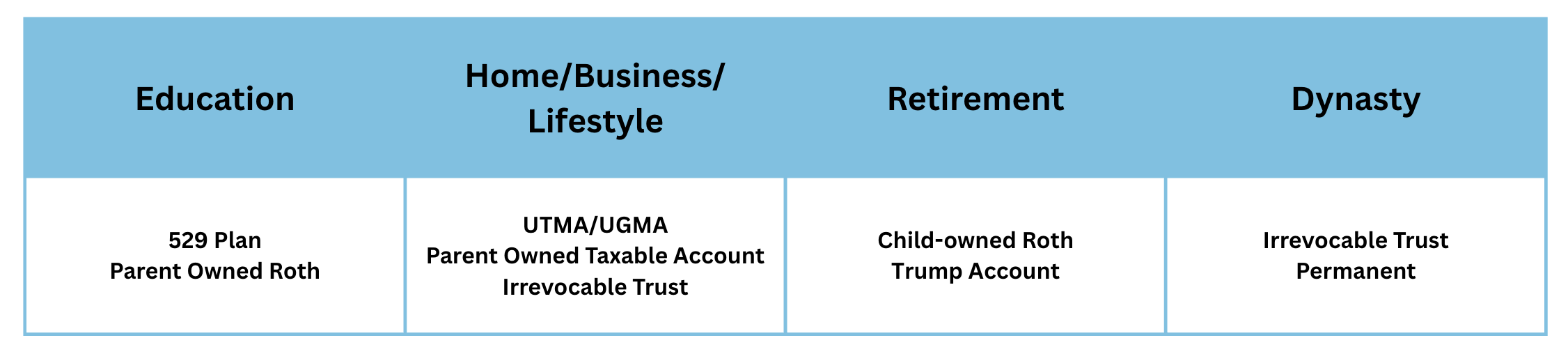

3. The CollegeInvest 529 Plan (The State Tax Offset)

- The Rule: Contributions can be made by anyone up to the gift tax exclusion limit ($19,000 in 2026).

- The Strategic Benefit: After maximizing the Roth IRA and the Trump Account, any remaining cash required for future higher education can be moved into a Colorado 529 plan. As the business owner, you claim a massive Colorado state income tax subtraction ($26,200 single / $39,200 joint in 2026), effectively driving down your local tax liability while cleanly funding their trade school or college path.

4. The Custodial Account / UTMA (The Intermediate Pool)

- The Rule: Governed by the Uniform Transfers to Minors Act, these are standard taxable brokerage accounts held in the child’s name under an adult custodian.

- The Strategic Benefit: UTMAs do not require earned income and have no contribution limits, though they are subject to the annual gift tax exclusion threshold. Use the UTMA as an intermediary clearinghouse to hold non-retirement, non-educational funds for major down payments (like a first car or a house at age 21). Additionally, remember the TA gift tax workaround: you can clear third-party funds through the UTMA first, then transfer them smoothly into the Trump Account to sidestep immediate Form 709 reporting requirements.

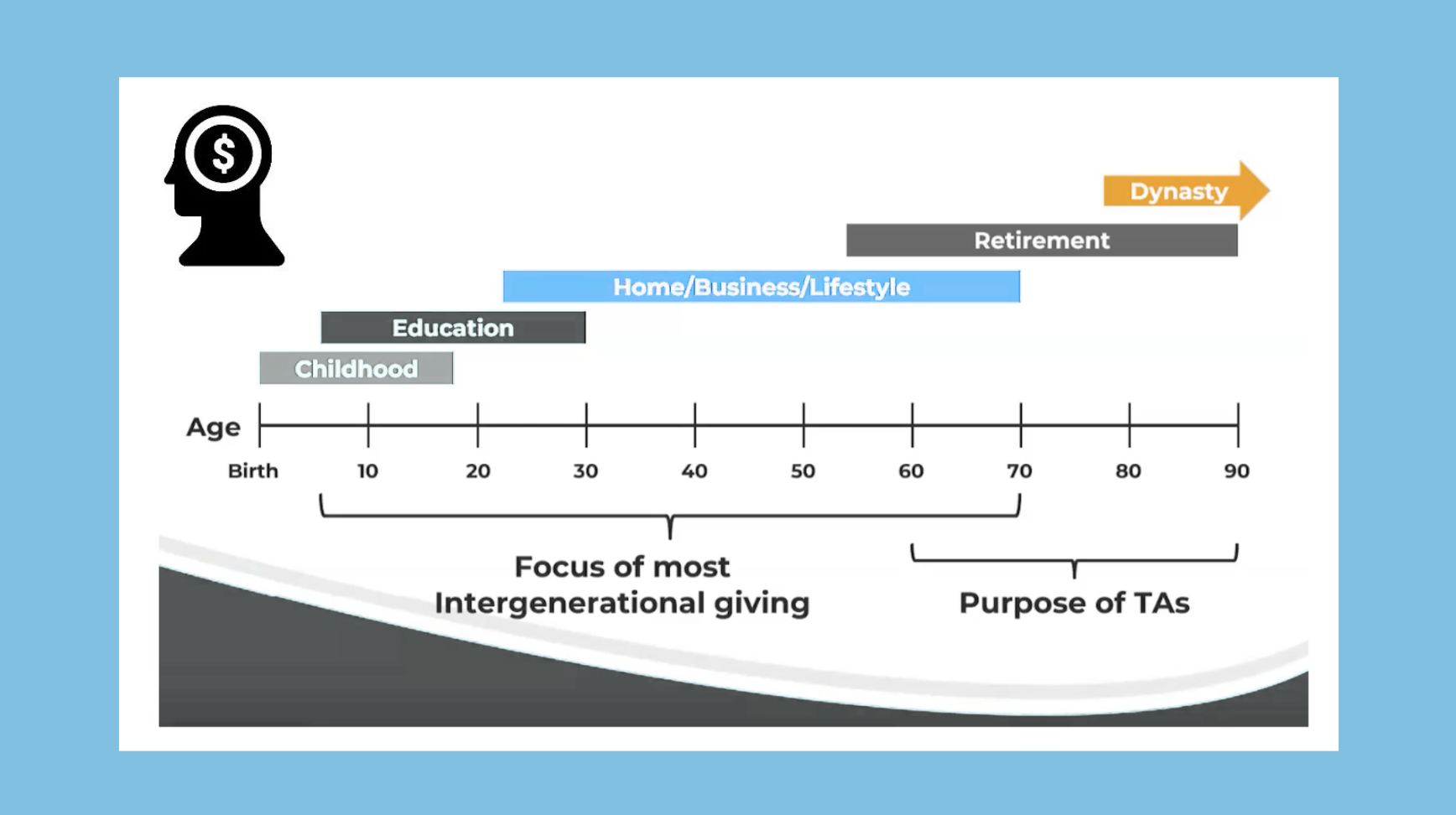

Summary of Tri-Factor Benefits

| Benefit Focus | How the Self-Employed Matrix Delivers |

| Taxes | Wipes out your highest marginal income tax bracket by shifting profit to your child’s 0% bracket. Eliminates FICA taxes on the child’s wages. Provides a massive Colorado state tax deduction via the 529 plan. |

| Savings | Uses the child’s unique time horizon to compound small sums. Fully funding a TA up to $5,000 a year from an early age can easily amass a substantial nest egg by the time they reach adulthood. |

| Setting Kids Up | Diversifies the child’s future asset pools: They get liquid college money (529), early adulthood flexibility (Roth IRA principal), a house/business pool (UTMA), and an armored retirement baseline (Trump Account). |