Audit

Organize

Formalize

Implementation

Monitor

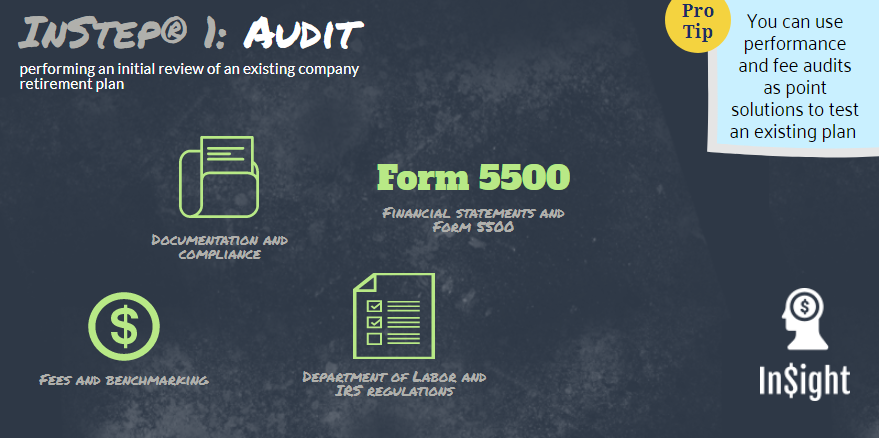

Audit

Our InStep® – Fiduciary Audit will focus on 4 areas: Our Accredited Investment Fiduciary (AIF®) will analyze and conduct a thorough audit to make sure the plan is operating within the guidelines of the plan-related documents. Documents will be reviewed in accordance with fi360’s prudent practice to make sure the financial information is reported correctly and the corporate plan is governed properly. A report will be prepared and delivered to the sponsor and investment committee upon completion.

Organize

In the Organize step, we start with education and documentation and reviewing salient parts of the audit. By knowing and following the rules, sponsors and their 401(k) participants expectations are met. Understanding and acknowledging roles, avoiding and if needed, properly managing conflicts of interest and protecting client assets is key from the outset. These are the steps that are included in the Organize step:

Formalize

The Formalize step is where we put the the Investment Policy Statement together. The IPS is the cornerstone of the rest of this program. Having a written, authoritative statement on how you govern the plan will prevent litigation and insulate the sponsor, company, and plan from harm and malfeasance. It is the single most important component to managing a plan. If you don’t have one, run, don’t walk to remedy this.

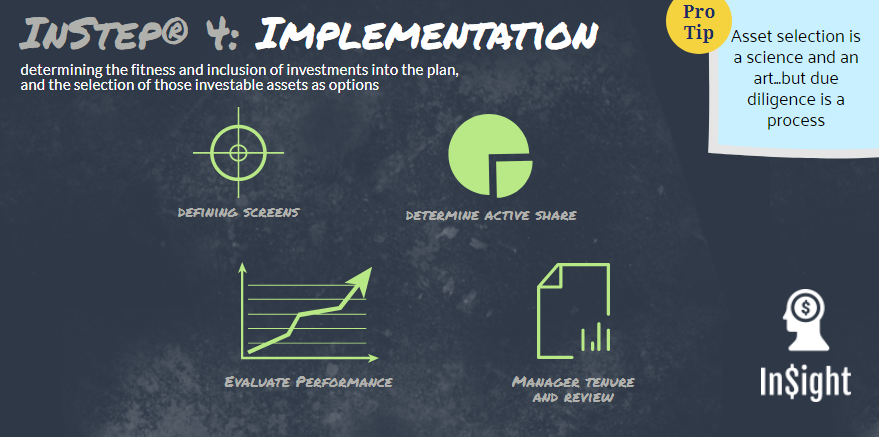

Implementation

Due diligence and documentation in the implementation stage is critical. In an effort to avoid confusion and contamination, down the road keep the IPS close by and follow the below screens to aid you in the decision making process. These elements will set a minimum acceptable criteria for choosing your investments and the manager.

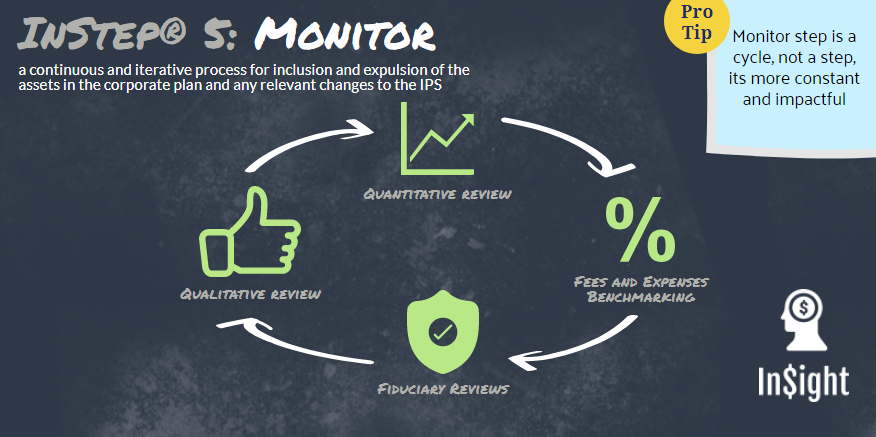

Monitor

The monitor step is the core fiduciary duty you’re responsible for. It’s where incongruence between your governance documents and your actions will cause breaches. This is where most advisors we replace have fallen off, largely because maintenance and monitoring are time consuming and there is no end. Remedies for this complacency include cycling investment committee members (noted in Organize), establishing a cadence for review, and setting priorities. Additionally, outsourcing the monitoring of the underlying assets to a third party advisor helps keep the process in check.