For individuals and families who have achieved a net worth exceeding $1 million in investable assets, financial management transitions from a task of accumulation to a complex challenge of preservation and strategic coordination. At this level of wealth, “standard” financial advice often proves insufficient. High-net-worth (HNW) investors require a sophisticated framework that integrates tax efficiency, estate transition, and risk mitigation into a singular, cohesive strategy.

Finding a financial advisor for millionaires requires more than a search for investment returns; it necessitates a partner capable of navigating the intricacies of the modern regulatory and tax landscape. Below are ten critical factors that HNW individuals should evaluate when selecting a wealth management firm in 2026.

1. A Rigorous Fiduciary Standard

While many professionals claim to act in a client’s best interest, a true fiduciary duty is a legal obligation that must be maintained at all times. For millionaires, the stakes of a conflict of interest are significantly higher. You should seek a Registered Investment Advisor (RIA) that operates under a rigorous fiduciary process that extends beyond the basic legal minimums. This commitment ensures that every recommendation, from asset allocation to insurance selection, is predicated solely on the objective of advancing your specific financial goals.

2. The InSight-Full® Planning Process

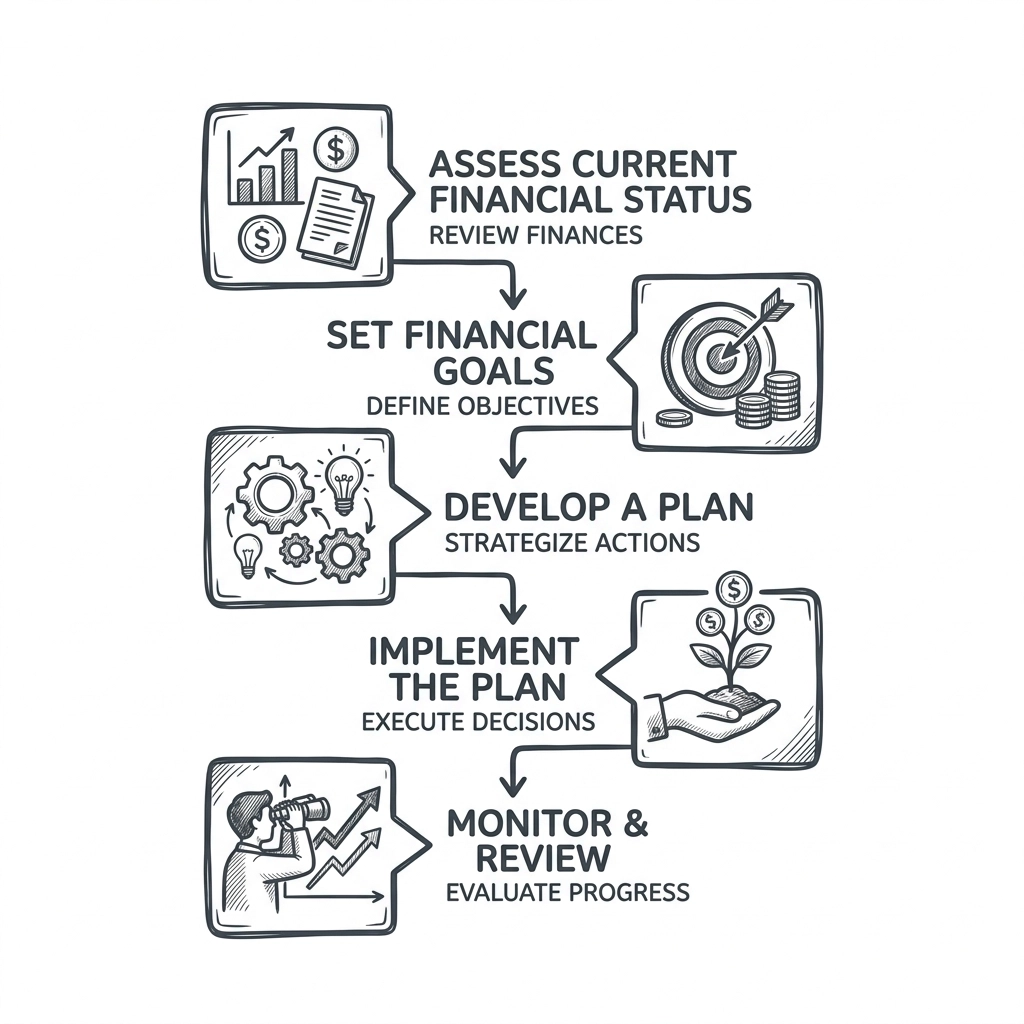

Sophisticated wealth management is not a series of disconnected transactions; it is a methodical, stage-gated process. At InSight Financial Planners, we utilize our proprietary InSight-Full® planning process to provide clarity and structure. This process is divided into five distinct stages:

- Discovery: A deep-dive analysis of your current trajectory, values, and long-term objectives.

- Organize & Formalize: The systematic categorization of all assets, liabilities, and legal documents.

- Agree: The collaborative finalization of the strategic roadmap.

- Implement: The disciplined execution of the agreed-upon strategies.

- Monitor: An ongoing monthly cadence to ensure the plan remains updated as tax laws and life circumstances evolve.

3. Integration of Six Core Planning Elements

Managing a million-dollar portfolio in isolation is a leading indicator of future inefficiency. A premier advisor must provide holistic expertise across six core planning elements:

- Investments: Tailored portfolio construction based on risk-adjusted returns.

- Taxes: Proactive strategies to minimize lifetime tax liability.

- Cash Flow: Optimization of liquidity and spending rates.

- Retirement: Ensuring sustainable distributions and longevity protection.

- Estate Planning: Coordinating the efficient transfer of wealth to future generations.

- Risk Management: Protecting assets through comprehensive insurance and contingency planning.

4. Expertise in 2026 IRS Contribution Limits

As of 2026, the Internal Revenue Service has adjusted contribution limits for qualified retirement accounts. A sophisticated advisor will ensure you are maximizing these vehicles to leverage tax-deferred or tax-free growth. For the 2026 tax year, key limits include:

- 401(k) / 403(b) Plans: The individual contribution limit is $24,500. For those aged 50 and older, the “catch-up” provision allows for a total contribution of $31,000.

- Individual Retirement Accounts (IRA): The annual limit is $7,000, with an increased limit of $8,000 for individuals aged 50 or older.

Properly navigating these limits is essential for high-income earners looking to reduce their taxable income while fortifying their retirement reserves.

5. Navigation of the “One Big Beautiful Bill” (OBBBA) Reforms

The legislative landscape shifted significantly following the implementation of the One Big Beautiful Bill (OBBBA) reforms in late 2025 and early 2026. A financial advisor for millionaires must be well-versed in these changes, particularly:

- 529 Plan Expansion: Enhanced flexibility for utilizing unused education funds.

- Health Savings Account (HSA) Adjustments: New thresholds for triple-tax-advantaged savings.

- Child Tax Credit Provisions: Structural changes that impact high-earning households.

Failure to adjust your strategy to these specific reforms can result in missed opportunities for tax optimization and wealth transfer.

6. A Team of Certified Financial Planner™ Professionals

Credentials serve as a baseline for competency. High-net-worth families should prioritize firms led by CFP® professionals. This designation signals that the advisor has met rigorous experience and ethical requirements and possesses the breadth of knowledge necessary to manage complex financial ecosystems. InSight Financial Planners operates with a team of CFP® experts, ensuring that every client receives advice grounded in professional excellence and technical proficiency.

7. Tax-Centric Investment Management

For the wealthy, it is not what you earn, but what you keep. Tax-centric investing involves sophisticated “asset location” strategies: placing tax-inefficient assets (like high-yield bonds) in tax-advantaged accounts while keeping tax-efficient assets (like index funds) in taxable brokerage accounts. Your advisor should provide a transparent view of your “Tax Alpha,” or the additional value created through proactive tax management.

8. Coordination of Estate and Business Succession

For many millionaires, a significant portion of their wealth is tied to a closely-held business or complex real estate holdings. An advisor must be capable of coordinating with your legal and tax professionals to ensure that your estate and business succession plans are documented and executable. This prevents the erosion of wealth through probate costs or unnecessary estate taxes.

9. Direct and Transparent Internal Workflows

Trust is built through clarity. An advisor should be able to explain their investment process and internal workflows without ambiguity. This includes how often they rebalance portfolios, the specific criteria used for manager selection, and how they communicate during periods of market volatility. Our structured 5-stage process ensures that clients always know where they stand and what the next milestone in their financial journey entails.

10. Focus on Long-Term Disciplined Partnership

The final thing to know is that successful wealth management is not a “set-and-forget” endeavor. It requires a disciplined partnership characterized by regular oversight and steady progress. A financial advisor for millionaires should act as a financial coach, providing the steady hand needed to remain focused on long-term goals despite short-term market noise. This partnership is built on the core values of Client First, Trusted Relationships, and Fiscal+Fitness.

Summary of Benefits

By selecting an advisor who adheres to these ten criteria, high-net-worth individuals gain:

- Stability: A structured approach that minimizes reactive decision-making.

- Control: A clear understanding of how every financial move impacts the overall plan.

- Efficiency: Maximizing the utility of every dollar through tax and cost optimization.

If you are seeking a higher standard of financial guidance, we invite you to experience the InSight-Full® difference.

Formal Disclosures:

InSight Financial Planners is a Registered Investment Advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.