Most likely yes.

Your financial and family situation will be the deciding factor.

If you’re single, have a large amount of savings, and no dependents then life insurance may not be for you. The reason being, unless your savings cannot pay for your debt(s) and that debt would be a burden on the person (most likely family) that takes it on then you don’t need life insurance.

Life insurance is typically purchased if you’re the primary provider for your dependents and spouse. For example, if you own a home with a mortgage and your significant other make 80% of your family’s income, how would you pay your mortgage if they were to unexpectedly pass? If you have kids, how would you support your family?

When people are young their debt is usually very high with student loans, car payments, mortgages, kids, etc so one major event or death would be devastating to a primary provider’s family.

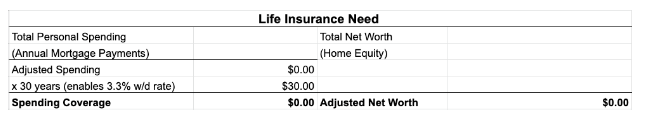

For assessing life insurance needs, InSight looks at this math:

Mortgage payoff + spending coverage – adjusted net worth = Life Insurance Need

The 30-year number enables us to be very conservative with our estimate and that is always adjustable. The 3.3% withdrawal rate is a safe estimate that the primary provider’s family can safely (withdraw a consistent amount without dipping into principal) for life.

Now the difference between permanent and term, how long you need the coverage, what riders you choose, etc will be up to your plan and goals and will need to be reviewed with a Financial Planner and Insurance Agent.

If you found this helpful please share it and/or leave a comment!