Once you’ve completed the other four elements (Audit, Organize, Formalize, and Implement) of the InStep® process, you will spend the majority of your time in the monitor phase. Your IPS will be in place, and the general questions about governance will be easy to answer. When you follow this process, you will spend less time and money navigating your plan because the policies you have in place, and the decision making matrix you have established.

The monitor step is the core fiduciary duty you’re responsible for. It’s where incongruence between your governance documents and your actions will cause breaches. This is where most advisors we replace have fallen off, largely because maintenance and monitoring are time consuming and there is no end. Remedies for this complacency include cycling investment committee members (noted in Organize), establishing a cadence for review, and setting priorities. Additionally, outsourcing the monitoring of the underlying assets to a third party advisor helps keep the process in check.

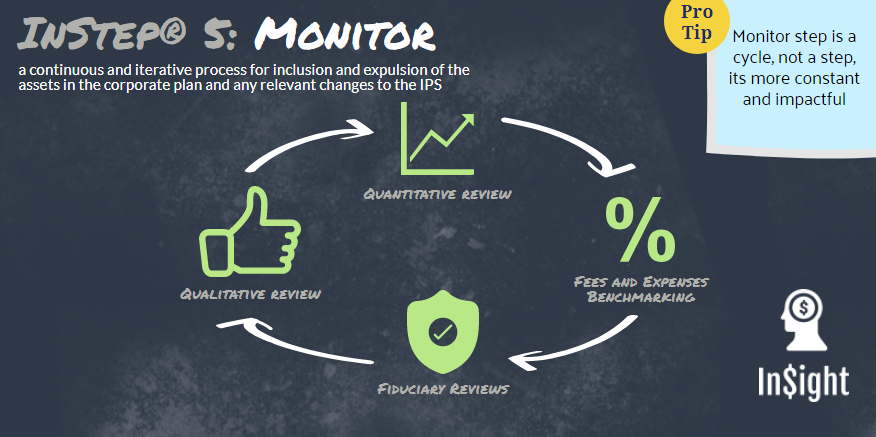

The four major pieces of this step are:

- Quantitative review

- Qualitative review

- Fees and Expenses Benchmarking

- Fiduciary Reviews

Quantitative Reviews

The qualitative review is designed to gain an intimate understanding of the success of the investments you chose, the valuation to their peers, and the correlation to the underlying objectives of the fund. Basically, it is focused on examining the performance of your chosen investment managers and then compares that performance to an appropriate index. Additionally, InStep® clients also review the peers of those managers and their relationship to the IPS.

Clients on the InStep® path generally position their InSight associate as their chief partner responsible for gathering and reporting on the quantitative metrics for the portfolio. The process for reviewing and reporting the performance of portfolio decisions should be consistent, routine, and objective.

This is mostly a number-crunching exercise combined with an understanding of your plans objectives. But our advisors truly demonstrate their value here because of their reporting expertise and ability to relate those metrics to your company’s IPS.

Qualitative Reviews

The qualitative review is an objective interpretation of the non-numeric changes to your portfolio assets. A systematic review of some leading indicators to performance that have not yet resulted in the change in the trajectory of your decisions. These may come from guidelines you established in the screening section of the implementation phase, or, they can be market news, and legally driven changes. They often include:

- Staff turnover and tenure shifts

- Organizational structure

- Level of service provided

- Quality of reporting

- Changes to lending practices

- Investment education

- News headlines

- Changes to the laws and fiduciary standards

Monitor Investment Expenses

The cornerstone of why most investment committees meet a source of issues as the practice unfolds. The challenge of balancing performance and expense is never ending, but for InStep® clients that have a vision for the plan and the process they intend to follow becomes a more manageable event.

Regulators and lawyers will spend more time reviewing the expenses that the plan absorbs more than any other single plan element. The scrutiny and exposure here is the greatest risk in plan administration. Plans must evaluate and account for investment-related fees, tax ramifications, compensation for services, and all other plan expenses.

The good news for InStep® clients who have a defined IPS is that they have defined parameters for evaluating fees and expenses. They can point to a process for reviewing fees and monitoring processes which satisfies their duty as fiduciaries. Those who don’t implement a process and monitor it as such will always be exposed to the risk of investments not performing as promised, failing their fiduciary responsibilities, and not meeting their investment returns for their employees and peers.

Fees are the biggest source of law suits and arbitration for plans. You should monitor the “going rates” for these four categories of fees and how your plans measure up. The four categories of fees are listed below:

- Investment or Money Manager: Fees and/or annual fund expenses

- Execution – Brokerage: Trading or processing costs (i.e. commissions, soft dollars, directed brokerage and 12b-1 fees)

- Consultant or Advisor: Consulting and administrative costs

- Custody – Recordkeeping: Custodial fees and transaction charges

Controlling for fees and uncovering conflicts of interest (noted in the Organize phase) are directly related. The simplest way to determine if a conflict of interest exists or is problematic is to follow the money. When you understand who is getting paid and for what services, then you have a clear picture of the plan and whether there are issues that need to be addressed.

What Is Fair and Reasonable?

This question is seemingly impossible to answer because it will always be relative. The key is to know “relative to what” and to follow the InStep® process.

Routinely managing a formal RFP process for select service providers, including the custodian, accountants, third party administrators, and investment managers is time consuming but a necessary part of the process. This keeps the investment committee and sponsor aware of prevailing services and monitor the prices the market offers those services. The RFP process draws the evaluators to as much of an apples-to-apples comparisons as possible.

There are two factors to consider when evaluating whether fees and expenses are reasonable.

- Can the fees be paid from the portfolio or plan assets? This must be considered from both a legal perspective and whether the organization itself will allow it.

- Are the fees reasonable considering the services provided?

InStep ® clients evaluate fees and services every three years, including our own services. This practice allows us to review the markets offerings, associated pricing for those fees, and demonstrates this due diligence in an orderly way. A lot can change in a three year period and having a cadence for monitoring these changes is critical to proper plan governance.

Cadence for Fiduciary Review (when to Monitor)

The fiduciary review is where you objectively evaluate your standing and where possible improvements and changes can be made. Since there’s a lot to consider at this step, here is a recommended schedule for you to use as a guide.

- Quarterly – Review overall portfolio and individual investment performance

- Annually – Review IPS, service providers, and your own fiduciary performance.

- Every three years – Revisit vendor contracts

The Process of Monitoring

You should anticipate fiduciary support that is objective, relevant, and makes the whole process easy on your team. The information you receive from the process should be rooted in an objective documented process that’s so well governed that any single component of the plan can be replaced and the rest of the system stays in compliance. Confidence in your corporate plan comes from a pattern of transparency and accountability, and not solely from investment performance. This is something that the InStep® process can control.